")

")

")

ZeroHedge, by Tyler Durden — April 13, 2020

Excerpt:

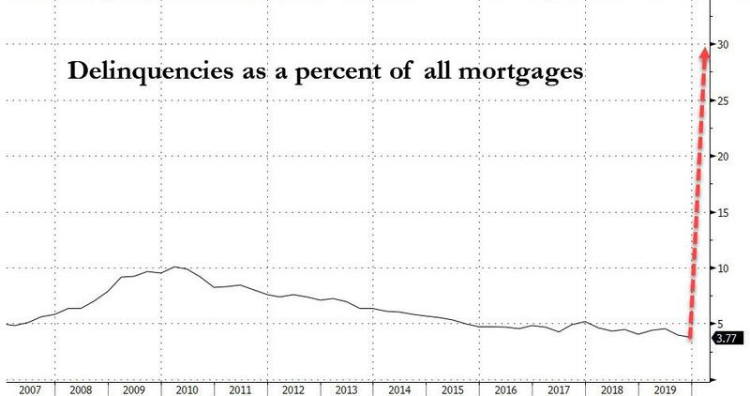

Earlier this week when we reported that JPMorgan has quietly halted all non-Paycheck Protection Program based loan issuance for the foreseeable future, we said that we didn’t buy the stated reason namely – the bank was drowning in (government-backstopped) applications and would be willing to forego millions in easy, recurring net interest income, and said that the real reason why JPMorgan would “temporarily suspend” all non-government backstopped loans such as PPP, is because the bank expects a default tsunami to hit, coupled with a full-blown depression that wipes out the value of assets pledged to collateralize the loans. We went on:

Furthermore, why issue loans that will default in months if not weeks, just as bankruptcy courts fill up with millions of cases (assuming the coronavirus clears out by then, as the alternative is simply unthinkable – a default tsunami without any functioning Chapter 11 or Chapter 7 process) when JPM can simply stick to the 100% risk-free issuance of government-guaranteed small-business loans which pay a handsome 1% interest, especially if it makes JPM look patriotic by doing its duty to bail out America.

Over the weekend our skepticism was confirmed when Reuters reported that JPMorgan, the country’s largest lender by assets and which will kick off earnings season tomorrow, will raise borrowing standards this week for most new home loans as the bank “moves to mitigate lending risk stemming from the novel coronavirus disruption.”

Starting Tuesday, customers applying for a new mortgage will need a credit score of at least 700, and will be required to make a down payment equal to 20% of the home’s value (something which we thought was the norm after the last financial crisis, but apparently lending conditions had eased quite a bit in the past decade).

……………………………………..

View the complete article including links and comments at: